ACA Health Insurance Options

Cutting through the Noise Saving Coloradans Millions in 2016

Originally published December 19, 2015 -- Guest Opinion in the Boulder Daily Camera>Return to Health Insurance Calculator

With the dissolution of Colorado HealthOP CO-OP insurance company, I am one of the ~83,000 Colorado residents and former CO-OP members who are scrambling to line up a new health insurance provider for 2016. This needs to be done during the open enrollment period which is from November 1st 2015 to January 31st 2016. The Colorado exchange, Connect for Health Colorado, has granted a "Special Enrollment" period to the Colorado HealthOP members allowing them to choose a new plan by December 31st and have insurance coverage begin on January 1st.

I began exploring the offerings on the exchange and found the range of options so intimidating that I worked up a spreadsheet to assist me in the decision process. My objective was to detail the total out-of-pocket annual cost of each plan at specified levels of actual medical expenses billed by providers. This total cost would be the sum of the annual insurance premiums paid plus the net payments that I would have to pay the providers (doctors, hospitals, labs, pharmacies, etc). The spreadsheet proved extremely helpful for my personal decision and turned up some curious anomalies.

Several of the companies provide numerous plans in each "metal" (Bronze, Silver, Gold, Platinum) category making selection that much more difficult, though once I compared those plans of the same "metal" category from the same insurance provider with the same network, I noticed that one of the plans would be superior at all levels of actual expenses over the other plans.

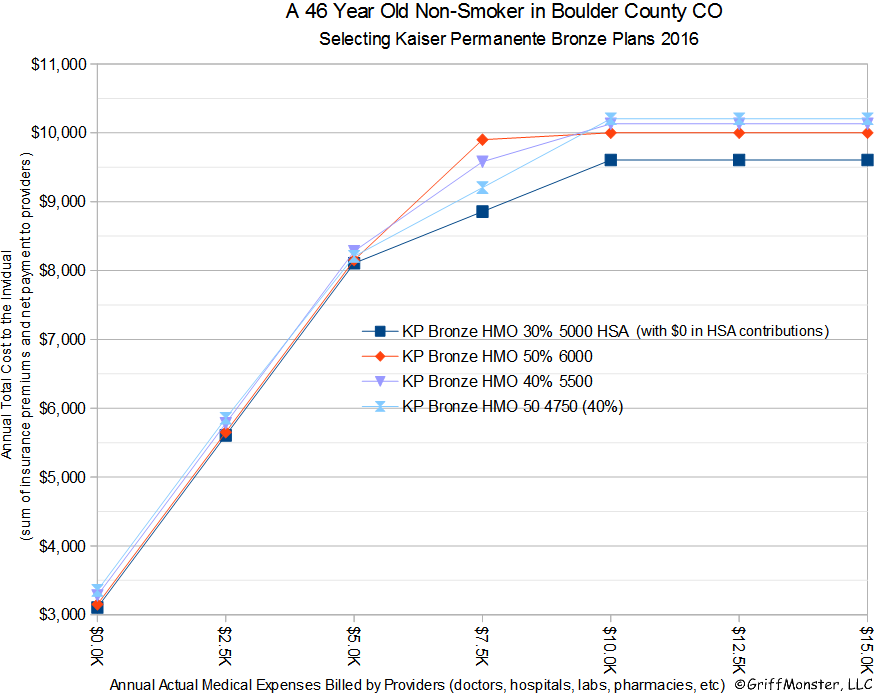

For example, Kaiser Permanente ("KP") offers four Bronze plans in Boulder County, with monthly premiums for a 46 year old non-smoker ranging from $258.83 to $279.58, yet the total out-of-pocket cost at all levels of actual medical expenses is always less for the "KP CO Bronze 5000/30%/HSA" plan which also has the lowest premium. I encourage anyone considering a KP Bronze plan to go with this option.

In order to determine which of the four KP Bronze plans was most cost effective, I compared all four plans using various estimated health expenditures. These included incurring no medical expenses, the classic $7,500 medical care situation example of having a baby with normal delivery (which all insurance companies must provide to allow you to compare coverage), and major medical expenses exceeding $10,000. In each of these scenarios, the plan I recommended provided the greatest savings from hundreds of dollars in premium savings alone to over a $1,000 for having a baby with no difference in services provided.

I'm encouraging KP and other insurance providers to simplify this process for us by deleting any plans that provide no additional benefits for the larger premiums charged. It is important that KP address this issue as they had ~35% of the Colorado exchange customers choose their plans in 2015 and are predicted to acquire a large share of the ~40% of exchange customers who had previously selected the Colorado HealthOP (who had the lowest cost Bronze plan in 2015).

For 2016, all four KP Bronze plans are cheaper than any other Bronze plan on the exchange, making the resolution of this confusion that much more relevant. With Bronze health plans being a popular choice -- 43% of last years Colorado HealthOP members selected a Bronze health plan -- this example alone may result in millions of dollars of additional costs to Coloradans in 2016. Examples such as these are just another reason why we need to consider changes to our current medical insurance system whether the ColoradoCare Amendment #69 (http://coloradocareyes.co/) option being offered to Coloradans on the 2016 election ballet or some other solution.

I reiterate, if you are going to go with a Kaiser Permanente Bronze and you live in Boulder County there is only one choice, the "KP CO Bronze 5000/30%/HSA" plan. More detailed information about the analysis, data sources, a graph for the KP Bonze plans in the example, and a calculator that allows you to analyze and compare between any health insurance plans you are considering can be viewed at http://www.ecolocate.org/health-insurance-calculator/

>Return to Health Insurance Calculator

Graph Comparing 46 Year Old Non-Smoker KP Boulder County Bronze Plans No HSA 2016

This issue is not unique to Kaiser Permanente or Colorado, note a similar example from Excellus Blue Cross Blue Shield ("BCBS") of NY

Graph Comparing Individual Tompkins County NY Excellus BCBS Plans No HSA 2016

Bonus Graphs that are not as obvious and don't require elimination of the plans or do they :)

Graph Comparing 46 Year Old Non-Smoker KP Boulder County Silver Plans No HSA 2016

Graph Comparing 46 Year Old Non-Smoker KP Boulder County Gold Plans No HSA 2016

Graph Comparing 46 Year Old Non-Smoker Anthem Boulder County Bronze Plans No HSA 2016

Details of Editorial Data Analysis

- 82,785 Colorado HealthOP members[CODORA15].

- More than 153,000 customers on the exchange in 2015 and more expected in 2016. [CHC1511]

- Expected enrollment for 2016 on the exchange is 217,000 customers and with Colorado HealthOp no longer an option and Kaiser having the least expensive plans on the market it is expected they will increase their portion of the Colorado exchange market.[LN15]

- In 2015 Colorado HealthOP had ~40% of the state health exchange and Kaiser had ~35% [HNC15]

- Colorado HealthOP Bronze plans represented 49.8% in 2014 and 43% in 2015 of plans purchased at the CO-OP[COHOP14][COHOP15]

- Open enrollment for health insurance runs from November 1st 2015 to January 31st 2016 [CHC1511]

- Connect for Health Colorado has granted a Special Enrollment period, an extension of the enrollment period to Colorado HealthOp and customers of a few other health plan members to Dec. 31st to enroll for Jan 1st, 2016 insurance. [CHC1512]

- Details and prices for the KP Bronze plans for Boulder County 46 year old non-smoker:[KP15]

(same plans and prices for Denver, Arapahoe, and Jefferson Counties) - $258.84 - KP Bronze HMO 30% 5000 HSA (Deductible $5,000|Max OPC $6,500|CO-Pay 30%)

- $262.57 - KP Bronze HMO 50% 6000 (Deductible $6,000|Max OPC $6,850|CO-Pay 50%)

- $273.36 - KP Bronze HMO 40% 5500 (Deductible $5,500|Max OPC $6,850|CO-Pay 40%)

- $279.58 - KP Bronze HMO 50 4750 (40%) (Deductible $4,750|Max OPC $6,850|CO-Pay 40%)

- Details and prices for the Excellus BCBS Bronze plans for Tompkins County Dep25:[NYSH15]

- $368.09 - Excellus BCBS Bronze Select NS INN Dep25 (Deductible $4,500|Max OPC $6,350|CO-Pay 50%)

- $391.97 - Excellus BCBS Bronze Standard HSA ST INN Dep25 (Deductible $4,000|Max OPC $6,450|CO-Pay 50%)

Many people who choose a Bronze plan are considering insurance as something they hope they will never need to use and have it as a safety net in case they have major medical bills. I compared the aforementioned KP Bronze plans assuming I would have no medical incidences for 2016 selecting this plan resulted in savings of $44.76, $174.24, and $248.88 for the year. The cost savings was the same for medical costs up to $4,750. I then checked the cost savings if incurring $7,500 in medical usage expenses which is the medical care situation example for having a baby with normal delivery that all insurance companies must provide to allow you to compare coverage across all the different plans available. The savings in this case for choosing the cheaper plan is $1,044.76, $724.24, and $348.88. The last comparison was for the major medical issue and I found that for anything over $10,000 the savings was $394.76, $524.24, and $598.88.

There are some specific details of these plans that make it more complicated to compare the plans but the effect of these differences are negligible on the consumer's cost. These include 3 primary care office visits for $50 per visit and variations on prescription drug rates. Some plans charge the same % after deductible as the plan while others have special $20 after deductible for generic drugs and another offers $25 generics before deductible.

References

- [CODORA15] Colorado Department of Regulatory Agencies. (2015, October 16). Division-of-Insurance-action-HealthOP

- [CHC1511] Connect for Health Colorado. (2015, October 30). Connect for Health Colorado Opens Downtown Denver Store Sunday to Launch Colorado's Third Open Enrollment for Individuals and Families.

- [CHC1512] Connect for Health Colorado. (2015, December 15). Connect for Health Colorado Special Enrollment Customers

- [HNC15] Health News Colorado. (2015, March 3). HealthOP edges out Kaiser, scores nearly 40 percent of exchange business.

- [LN15] Louise Norris. (2015, December 1). Colorado health insurance exchange / marketplace

- [KP15] Kaiser Permanente. (2015, December 15). Individual and Family Plans - Compare 2016 Plans for non-smoking 46 ye ar old

- [COHOP14] Colorado HealthOP Annual Report 2014 (2014, November)

- [COHOP15] Colorado HealthOP Annual Report 2015 (2015, October)

- [NYSH15]New York State of Health. (2015, December 15). NY State Health Exchange.